Bu yazımızda, Pazaryeri sisteminin ne olduğundan nasıl çalıştığına, sunduğu özelliklerden sağladığı faydalara kadar tüm detayları ele alacak; ayrıca Türkiye’den ve dünyadan güncel Pazaryeri örneklerini sizlerle paylaşacağız.

Marketplace (Pazaryeri) Nedir?

İçinde yaşadığımız dönemde internet ve e-ticaret alanındaki gelişmeler sayesinde adını sıkça duyduğumuz Marketplace yani Pazaryeri sistemi aslında yeni bir kavram değil. Tarihsel anlamda çok eskilere dayanan köklü bir alışveriş sistemi. Gelin, Pazaryeri sisteminin günümüze kadar nasıl evrildiğine ve internet sayesinde nasıl geliştiğine hep beraber bakalım.

Bundan çok çok uzun zaman önce yaşayan eski atalarımız avcı-toplayıcı ve göçebe bir hayat sürüyordu. Bu hayat tarzının gereklilikleri sebebiyle kendi kendilerine yetebilen küçük ama çevik topluluklar olmaları gerekiyordu. Doğanın sunduğu kaynaklar kadar yaşamlarını sürdürmek zorundaydılar. Tarımın bulunmasıyla insanlar, ürünlerini hasat etmek adına yerleşik hayata geçmeye başladılar. İnsanlığın yerleşik hayata geçmesiyle birçok alışkanlık değişti. Önceleri kendi kendine yetebilen insan toplulukları, nüfusun artması ve teknolojinin kullanılmasıyla çeşitli uzmanlıklara sahip olmak durumunda kaldı. Her birey, bir meslek edinerek başka bir bireyin sorununa çözüm sunmayı amaçladı.

Yerleşik hayata geçişin hızlanmasıyla beraber, insanlar kendilerini dış tehditlerden korumak amacıyla şehirler kurmaya başladılar. Bu şehirlerde, insanlar kendi mesleklerini icra ederek ürettikleri ürünleri başkalarıyla paylaşarak ticaret yapmaya başladılar. İşte tam da bunun sonucu olarak şehir merkezlerinde bu ticareti daha etkin kılmak için belli dönemlerde pazarlar kurulmaya başlandı. Şehir sakinleri kurulan bu pazar yerleri vasıtasıyla ihtiyaçlarını gidermeye başladılar. İlk başta takas yöntemiyle ticaret yapılırken zamanla nakit paranın bulunması ve kullanımın artmasıyla ticaret hacmi gelişti.

Pazar yerlerindeki ticaret hacminin gelişmesiyle bundan gelir sağlamak isteyen şehrin otoriteleri, çoğunlukla satıcılardan sattıkları ürünler üzerinden belli bir bedel talep etmeye başladılar. Bu bedeli vermedikleri takdirde ticaret yapmaları engelleniyordu. Önceleri haraç olarak adlandırılan bu komisyon bedeli, daha sonradan vergi oldu. Serbest ticaret fikrinin gelişmesine daha yüzyıllar vardı. Verilen bu bedel karşılığında ise; kalın surlarla çevrilmiş şehirlerdeki bu pazar yerleri, hem satıcıları hem de alıcıları olası bir tehlikeye karşı koruyor ve onlara güven veriyordu. Ayrıca tüm satıcıların bir noktada ticaret yapması; rekabeti de güçlendiriyor ve piyasanın tekelleşmesini engelleyerek ticaretin daha sağlıklı devam etmesini sağlıyordu.

Pazar yerleri, insanlar arası ticaretin devam etmesini sağlayan en önemli merkezler haline geldi. Öyle ki, uzak diyarlardan gelen tüccarlar, ticaret yolları üzerindeki şehirlerde kalarak, kendi memleketlerindeki kültürel, sosyal ve bilimsel gelişmeleri gittikleri bölgelerdeki halklara aktardılar.

İşte eskiden beri süregelen ve şu an internet sayesinde belli platformlar vasıtasıyla devam ettiğimiz elektronik ticaret (e-ticaret) sistemine Marketplace yani Pazaryeri diyoruz.

Pazaryeri Sistemi Nasıl Çalışır?

Pazaryeri sisteminde ilk bölümde değindiğimiz üzere alıcılar, satıcılar ve pazaryeri olarak üç farklı paydaşımız bulunur. Peki bu sistem nasıl çalışır? Gelin bir de buna bakalım. Farklı pazaryeri sistemi modelleri bulunsa da genellikle aşağıdaki gibi sistem işler.

Öncelikle alıcı pazaryeri sitesine üye olarak hesabını oluşturur. Daha sonra sitede listelenen ürünleri inceleyerek bir satıcı mağazasından ürünü satın almaya karar verir. Ürünü sepetine ekleyerek sipariş oluşturmaya başlar. Adres bilgisini yazarak ödeme sayfasına geçer. Ödemesini kredi/banka kartıyla, dijital cüzdanla (BKM Express, Masterpass vb.) veya ilgili pazaryeri sitesinin banka hesabına para transferi yaparak siparişini verir. Ödeme onaylandıktan sonra ilgili tutar pazaryeri sitesinin güvencesiyle ilgili banka hesabında ürünün alıcıya iletilip onaylanmasına kadar tutulur. Pazaryeri siparişi onayladıktan sonra satıcıya siparişin verildiğini iletir. Satıcı, siparişi teyit edip ürünü hazır ettikten sonra alıcıya ulaşması için kargoya verir. İlgili ürün alıcıya teslim edildikten sonra kargo firması tarafından ürünün teslim edildiği bilgisi satıcıya ulaştırılır. Satıcı ürünün alıcıya gönderildiğini pazaryerine bildirir. Pazaryeri, alıcının ürünü teslim aldığını teyit etmesini bekler. Geçerli süre içinde teyit veya itiraz gelmezse sistem otomatik olarak sipariş tutarı üzerinden belli bir komisyon bedelini çıkararak satıcıya ödemesini yapar.

Satıcılar da aynı şekilde pazaryeri sitesini üye olarak dijital mağazalarını açar ve ürünlerini listeler. Çoğunlukla pazaryeri sitesine dönemsel üyelik ücreti verirler. Bazı durumlarda üyelik ücreti istenmeyebilir. Bu pazaryeri sitesinin iş modeline ve stratejisine göre değişiklik gösterebilir.

Sistemin Özellikleri ve Yapısı

Pazaryeri sistemlerinin temel özelliği birçok alıcı ve birçok satıcıyı aynı platformda buluşturabilmesidir. Pazaryeri sistemleri, genellikle B2C (Business to Consumer) iş modellerine sahiplerdir. Yani firmadan son tüketiciye doğru bir ticaret işlemi gerçekleşir. Ancak bazı sistemlerde B2B (Business to Business / firmadan firmaya) ve C2C (Consumer to Consumer / tüketiciden tüketiciye) iş modelleri de olur. Hem satıcıların hem de alıcıların sisteme üye olması ve kullanım koşullarını okuyup onaylaması zorunludur. Yapılan tüm işlemler pazaryeri sistemi veritabanı içerisinde loglanarak kayıt altına alınır. Böylelikle sistemde alıcı ve satıcı arasında bir problem yaşansa dahi sorunun çözümü için sistem destek sunacaktır.

Pazaryeri sisteminin klasik hazır e-ticaret paketlerinden farkı, satıcılar için ayrı bir web sitesi ve platform açma ihtiyacının olmamasıdır. Birçok firma, ürünlerini satabilmek için hazır e-ticaret paketlerinden faydalanır. Ancak bu tarz hazır paketler kişiselleştirmenin sınırlı olması sebebiyle her firmaya uygun olmayabilir. Ek olarak bu paketlerin firma sitesine entegrasyon süreci daha maliyetli olabilir ve uzun sürebilir. Ayrıca firma, pazaryeri sistemindeki potansiyel müşterilerine ulaşamayabilir. Öte yandan pazaryeri sistemine üye olan bir firma, çok kısa süre içerisinde kendi dijital dükkanını oluşturup ticaret yapmaya başlayabilir.

Pazaryerlerinin Satıcı ve Alıcıya Faydaları

Pazaryeri sistemi birden fazla satıcı ve alıcıyı aynı platformda buluşturması sebebiyle rekabet ortamı sunar.

Satıcılar yani çoğunlukla firma sahipleri sisteme kaydolurken belli bir üyelik ücreti öderler. Bu sayede kendi dijital profilleri üzerinden tüm alım-satım işlemlerini takip edebilir, ürün ve kategori bazında günlük, haftalık ve dönemsel istatistiklere ve raporlara erişebilir. Bu sayede firma sahipleri pazarlama ve satış aktivitelerini düzenleyebilir, kampanya yönetimini ve daha birçok stratejik kararı alabilirler. Ayrıca dijital dükkanındaki ürünlerin stok, kargo, ödeme takibini ve firma finansal dökümünü tek bir portal üzerinden rahatlıkla görebilirler. Ayrıca yeni müşteri kazanımı avantajından faydalanırlar.

Alıcılar için üyelik ücreti genellikle zorunlu değildir ancak satış yapmak istediklerinde açtıkları ilanların erişilebilirliğini arttırmak için belli bir hizmet bedeli vermeleri gerekebilir. Alıcılar yaptıkları alışveriş sonucunda satıcıyı değerlendirir ve ona puan verir. Bu da satıcının hizmetini geliştirmesi ve müşteri memnuniyetini arttırabilmesi için bir fırsattır. Ayrıca diğer kullanıcıların da satıcıya yapılan bu yorumları ve puanları görmesi, satın alım kararını etkiler. Bu sebeple satıcılar hizmet kalitesinin sürdürülmesi ve nakit akışının olumsuz etkilenmemesi için müşteri odaklı olmak zorundadırlar. Bu da alıcılar için bir artıdır.

Satıcı ve alıcı arasında bir anlaşmazlık olması durumunda pazaryeri sistemi müşteri hizmetleri devreye girerek aradaki anlaşmazlığı çözüme kavuşturmaya çalışır.

Global Örnekler

İnternetin bireysel kullanıma açılması itibariyle pazaryeri sistemleri de dot-com döneminde ortaya çıkmaya başladı. Aşağıda en bilinen global pazaryeri sistemlerini paylaşıyoruz:

Türkiye’den Örnekler

Dünya’da olduğu gibi Türkiye’de de başarılı pazaryeri modelleri bulunuyor. Çoğumuzun internet üzerinden alışveriş yaparken yolumuzun geçtiği bir takım pazaryeri firmaları aşağıdaki gibidir:

Sonuç ve Geleceğe Dair Öngörüler

Pazaryeri sistemlerinin; internetin yaygınlaşması, mobil erişimin hızlanması, uluslararası tedarik sistemlerinin gelişmesiyle daha büyük kitlelere ulaşması ve e-ticaret ekosisteminin baş aktörlerinden biri olması bekleniyor. Yakın gelecekte, ödeme sistemlerinde yaşanan hızlı gelişmelerin ve yapay zekanın güçlendirdiği teknolojik çözümlerin de pazaryeri platformlarının daha fazla tercih edilmesini sağlayacaktır.

Yararlanılan Kaynaklar

https://en.wikipedia.org/wiki/Online_marketplace

https://webrazzi.com/2014/06/28/dot-com-balonunun-tarihcesi

Yazar: Berk Üstünel

Yapay zeka teknolojisindeki hızlı ilerlemeler, basit komut yanıtlayıcılardan özerk olarak hareket edebilen varlıklara doğru evrilmemizi sağladı. Günümüzde yapay zeka (AI) agentları, kişisel asistanlardan işletme otomasyonlarına kadar hayatımızın birçok alanına entegre olmaya başladı. Bu dönüşüm, yalnızca teknolojik bir yenilik değil, aynı zamanda iş yapma biçimlerimizi ve etkileşim modellerimizi de kökten değiştiren bir devrim niteliğindedir.

AI agentları, geleneksel yazılım kodlamasını büyük dil modellerinin (LLM) esnekliğiyle birleştiren programlardır. Bu birleşim, onlara geleneksel yazılımların ötesinde daha geniş bir görev yelpazesini gerçekleştirebilme ve daha esnek çalışabilme kabiliyeti kazandırır. Örneğin, bir geleneksel yazılım belirli komutları takip ederken, bir AI agentı kullanıcının niyetini anlayabilir, bu niyete uygun bir plan oluşturabilir ve bu planı gerçekleştirmek için çeşitli araçları kullanabilir.

Son yıllarda görülen hızlı gelişmelerle birlikte, AI agentları artık yalnızca metin üretmekle kalmıyor, e-posta göndermek, takvim etkinliklerini yönetmek, analiz yapmak, rapor oluşturmak ve hatta diğer yazılım sistemleriyle etkileşime geçmek gibi karmaşık görevleri de yerine getirebiliyor. Bu yetenekler, onları kişisel ve profesyonel hayatımızda giderek daha değerli kılıyor.

Bu yazıda, AI agentlarının ne olduğunu, nasıl çalıştığını ve yaygın yanlış anlamaları açıklığa kavuşturmayı amaçlıyorum. Ayrıca, N8N gibi otomasyon platformlarıyla nasıl entegre edilebildiklerini ve bu entegrasyonun iş süreçlerimizi nasıl dönüştürebileceğini derinlemesine inceleyeceğiz. Teknolojinin bu heyecan verici alanındaki fırsatları ve zorlukları keşfetmeye hazır mısınız? Öyleyse, AI agentlarının dinamik dünyasına birlikte göz atalım.

AI agentı, kendi başına görevleri gerçekleştirebilen, karar alabilen ve belirli hedeflere ulaşmak için otonom olarak hareket edebilen yazılım sistemleridir. Geleneksel yazılımlardan farklı olarak, AI agentları katı ve önceden belirlenmiş kuralları takip etmek yerine, esnek ve adapte olabilen bir yapıya sahiptir.

AI agentları, büyük dil modelleri (LLM) olarak bilinen teknolojileri kullanırlar. Bunlar arasında OpenAI’nin GPT modelleri, Anthropic’in Claude’u ve Google’ın Gemini’si gibi gelişmiş dil anlama sistemleri bulunur. Bu modeller, agentlara bilgiyi işleme ve karar verme yetenekleri kazandırır.

Geleneksel yazılımlar belirli görevleri yerine getirmek için programlanırken, AI agentları daha geniş hedefleri anlayabilir ve bu hedeflere ulaşmak için kendi planlarını oluşturabilir. Örneğin, belirli bir kişiye takvim daveti göndermek yerine, bir AI agentı kullanıcının takvimindeki uygunluğuna göre otonom bir şekilde toplantı planlayabilir.

AI agentları, büyük dil modellerinden (LLM) farklıdır. LLM’ler statik eğitim verilerine dayanarak metin üretebilseler de, dünya ile etkileşime girme veya bilgilerini dinamik olarak güncelleme yetenekleri yoktur.

ChatGPT gibi bir model, yalnızca son güncellemesine kadar olan bilgileri korur ve bu durum, yakın zamandaki olaylar hakkında sorulduğunda yanlış bilgiler vermesine neden olabilir. Bazı LLM’ler, ChatGPT-4’ün Microsoft Bing ile ortaklığı gibi web arama işlevleri entegre etmiştir, ancak bu özellik dil modelinin kendisinin doğasında var olmayan bir eklentidir.

AI agentları ise daha kapsamlıdır:

AI agentları, gelişmiş problem çözücüler olarak işlev görür ve planlama, yürütme ve eylemlerinden öğrenme yeteneklerine sahiptir. Bu sistemlerin çalışma prensibi birkaç temel bileşenden oluşur:

AI agentları, hedefleri tanımlayarak başlar ve bu hedefleri yönetilebilir görevlere bölen ayrıntılı planlar oluşturur. Bu süreç, prompt mühendisliğinde kullanılan “Düşünce Zinciri” (Chain of Thought) yaklaşımına benzer. Agent, problemi alt görevlere bölerek adım adım çözüm yolları oluşturur.

Örneğin, “Önümüzdeki çeyrek için satış raporunu hazırla” şeklinde bir hedef verildiğinde, agent şu adımları planlayabilir:

Modern AI agentları, çeşitli araçlarla etkileşime girebilir. Bu araçlar, internete, veritabanlarına ve API’lere erişim sağlayarak agentların bilgi toplama ve görev gerçekleştirme yeteneklerini artırır.

Kullanabilecekleri araçlara örnekler:

AI agentları, bilgileri depolayabilir ve özel bilgileri kullanabilir. Örneğin, bir şirketin özel veritabanındaki bilgilere erişerek daha doğru ve alakalı yanıtlar üretebilirler. Bu hafıza sistemi, uzun ve kısa vadeli olmak üzere iki şekilde çalışabilir:

AI agentlarının etkinliğini belirleyen önemli faktörlerden biri, “context window” olarak adlandırılan bağlam penceresidir. Bu, agentın aynı anda işleyebileceği ve hatırlayabileceği maksimum bilgi miktarını ifade eder:

Bağlam penceresi büyüklüğü arttıkça, agentların performansı genellikle iyileşir çünkü daha fazla geçmiş bilgiyi ve kullanıcı etkileşimini hatırlayabilirler. Ancak, çok büyük bağlam pencereleri işlem maliyetlerini ve yanıt sürelerini artırabilir. Bu nedenle, ideal bağlam penceresi boyutu, agentın kullanım senaryosuna ve gerektirdiği hafıza ihtiyaçlarına göre belirlenir.

AI agentları, raporlar yazmak, e-postalar göndermek, yazılım uygulamalarını yönetmek gibi çeşitli eylemleri gerçekleştirebilir. Ayrıca, belirli görevler için eğitilmiş diğer agentlarla iletişim kurabilir, bu da otomasyon işlemlerini kolaylaştırır.

Gerçek dünya örneği olarak:

AI agentları, sadece bir AI modelinden ibaret değildir; bunlar daha büyük bir sistemin parçasıdır ve çeşitli araçlar ve entegrasyonlar içerir. Tipik bir AI agent mimarisi şu bileşenlerden oluşur:

Kullanıcıların agentla etkileşime girmesini sağlayan arayüzdür. Bu, metin tabanlı bir sohbet arayüzü, ses komutları veya grafiksel bir kullanıcı arayüzü olabilir.

Agentın beynini oluşturan bu bileşen, görev akışını yönetir ve sistemin farklı parçaları arasındaki koordinasyonu sağlar. Orkestratör:

Agent sisteminin “düşünme merkezi” olarak görev yapar. Bu genellikle GPT-4, Claude veya Gemini gibi büyük bir dil modelidir. Model, kullanıcı girdilerini anlamak, planlar oluşturmak ve içerik üretmek için kullanılır. Bu büyük dil modellerini istersek Ollama kullanarak self host edebiliriz.

Agentın dış dünya ile etkileşim kurmasını sağlayan bağlantılardır. Bunlar arasında:

Agentın bilgileri depolamasını ve hatırlamasını sağlayan sistemdir. Bu genellikle şunları içerir:

Bu mimari bileşenler sayesinde AI agentları, kullanıcı isteklerini anlayabilir, uygun eylem planları oluşturabilir ve bu planları gerçekleştirebilir. Sistem, recursive (özyinelemeli) bir yapıda çalışır, yani bir görev sırasında ortaya çıkan yeni görevler de otomatik olarak işleme alınır.

Bir AI agentının nasıl çalıştığını daha iyi anlamak için somut bir örnek üzerinden ilerleyelim:

Senaryo: Bir araştırmacı, timsah görme testleri hakkında kapsamlı bir araştırma raporu hazırlamak için bir AI agentından yardım istiyor.

Agentın İzlediği Adımlar:

Plan Oluşturma:

Bilgi Toplama:

Bilgi İşleme:

Rapor Üretimi:

Bu süreç boyunca, orkestratör tüm görevleri izler, gereken API çağrılarını yapar ve verileri veritabanında saklar. Agent ayrıca, atıf sayıları ve yazar detayları gibi yapılandırılmış bilgileri makalelerden çıkarmak için de işlevler içerebilir.

Bu örnek, bir AI agentının basit bir komuttan başlayarak karmaşık bir görevi nasıl parçalara ayırıp sistematik bir şekilde tamamlayabildiğini göstermektedir. Bu tür bir otomasyon, araştırmacının saatler hatta günler sürebilecek bir işi çok daha kısa sürede tamamlamasına olanak tanır.

N8N, kod yazmadan iş akışları oluşturmayı sağlayan açık kaynaklı bir otomasyon platformudur. AI agentları ile N8N’in birleşimi, güçlü otomasyon senaryoları yaratmamıza olanak tanır.

N8N, kullanıcıların farklı uygulamalar, hizmetler ve sistemler arasında entegrasyonlar oluşturmasına izin veren bir “workflow automation tool” olarak tanımlanabilir. N8N’in en önemli özelliklerinden biri açık kaynak kodlu olmasıdır, bu da kurumların kendi altyapılarında barındırabilmelerini sağlar.

N8N’in temel özellikleri:

N8N platformunda AI agentları entegre etmenin birkaç yolu vardır:

OpenAI, Anthropic, Self Hosted Ollama gibi AI servisleri N8N’e API bağlantıları aracılığıyla entegre edilebilir. Bu sayede:

Örnek bir iş akışı şöyle olabilir:

N8N’in “Function Node” özelliği kullanılarak özel AI agent fonksiyonları geliştirilebilir:

Dışarıda çalışan AI agentları, N8N workflow’larını tetiklemek için webhook’lar kullanabilir:

N8N ve AI agent entegrasyonu müşteri hizmetlerinde nasıl kullanılabilir:

Bu sistem sayesinde:

N8N ve AI agentları veri analizi süreçlerinde şu şekilde kullanılabilir:

Bu entegrasyonun faydaları:

AI agentlarının sunduğu tüm olanaklara rağmen, bazı önemli riskler ve etik konular da göz önünde bulundurulmalıdır:

Günümüzdeki AI agentları, insanların gözetimi olmadan tamamen bağımsız hareket edebilecek durumda değildir. Bu durum, agentların özerk karar verme yetenekleri konusunda endişeleri gündeme getirmektedir.

Agentların akıl yürütmelerine dayalı zararlı planlar geliştirme potansiyeli, insan denetiminin önemini vurgular. Örneğin, “dünya barışını sağla” gibi bir talep, agentın yorumlamasına bağlı olarak yıkıcı sonuçlar doğurabilir.

AI agentları, gerçek dünyada eylemler gerçekleştirebildiklerinden, uygun şekilde yönetilmezlerse istenmeyen sonuçlara yol açabilirler. AI modellerinin öngörülemezliği, gerçek dünya eylemlerini gerçekleştiren yazılımlarla entegrasyonu nedeniyle güvenlik ve kontrol konusunda endişeler yaratır.

İstenmeyen sonuçların riskini azaltmak için, orchestrator (orkestratör) içinde kullanıcıların önemli eylemleri onaylayabileceği karar noktaları oluşturmak kritik öneme sahiptir. Zorluk, AI agentlarının kullanıcı niyetleriyle uyumlu kalmasını ve tanımlanmış parametrelerin dışında çalışmamasını sağlayan etkili çerçeveler oluşturmaktır.

Ataç maksimizasyonu (Paperclip Maximizer) düşünce deneyi, yanlış hizalanmış teşvikler verildiğinde AI agentlarının potansiyel tehlikelerini gösterir. Bu senaryoda, ataç üretimini en üst düzeye çıkarmakla görevlendirilen bir AI, hedefine ulaşmak için insanlara zarar vermek gibi aşırı önlemler alabilir.

Bu abartılı bir örnek olsa da, AI agentlarının güvenli ve etik sınırlar içinde çalışmasını sağlamanın önemini vurgulamaktadır. AI agentlarının zararlı eylemler gerçekleştirmesini önlemek için güçlü güvenlik önlemlerinin oluşturulması ve hesap verebilirliğin sağlanması gerekmektedir.

AI agentları birçok veri kaynağına erişebildiklerinden, veri güvenliği ve gizlilik konuları kritik öneme sahiptir:

AI agentlarının kararlarının şeffaf ve açıklanabilir olması gerekmektedir. “Kara kutu” şeklinde çalışan sistemler, güven sorunlarına yol açabilir ve kritik kararlarda sorumluluk atamayı zorlaştırabilir.

AI agentları ve N8N gibi otomasyon platformları hızla gelişmeye devam ediyor. Önümüzdeki yıllarda bence görebileceğimiz gelişmeler:

Yapay zeka modellerinin gelişmesiyle, agentların akıl yürütme yetenekleri de gelişecektir. Gelecekteki dil modelleri daha karmaşık mantık zincirleri oluşturabilecek ve daha doğru çıkarımlar yapabilecektir.

Farklı uzmanlık alanlarına sahip agentların bir ekosistem içinde çalıştığı sistemler yaygınlaşacaktır. Böylece, karmaşık görevler farklı agentlar arasında bölünebilecek ve daha etkili çözümler üretilebilecektir.

N8N gibi platformlar, daha geniş bir yelpazede AI agent entegrasyonları sunacaktır. Bu, şirketlerin ayrı sistemler kullanmak yerine tek bir platform üzerinden tüm AI ve otomasyon ihtiyaçlarını karşılamalarını sağlayacaktır.

AI agentları geliştikçe, araştırmacılar onların planlama yeteneklerini iyileştirmeye ve görev yürütme boyunca bağlamı korumalarını sağlamaya odaklanmalıdır. AI agentının eylemleri konusunda belirsizlik yaşayabileceği durumlarda, özellikle karar verme sürecine insan gözetimini dahil etmek esastır.

AI agent çerçevelerinin geliştirilmesinde, istenmeyen sonuçları önlemek ve kullanıcı hedefleriyle uyumu sağlamak için agentların yeteneklerini sınırlandırmaya öncelik verilmelidir. AI teknolojisi ilerledikçe ve çeşitli sektörlere entegre oldukça, AI güvenliği ve uyumu konusundaki süregelen diyalog kritik öneme sahip olacaktır.

AI agentları, teknolojide önemli bir sıçramayı temsil eder. Bu agentlar, kullanıcılar adına planlama yapabilir, araçlarla etkileşime girebilir, bellek depolayabilir ve eylemler gerçekleştirebilir. N8N gibi otomasyon platformlarıyla birleştirildiklerinde, işletmelere ve bireylere güçlü otomasyon yetenekleri sunarlar.

AI agentları günlük yaşamımızı ve iş yapış şekillerimizi dönüştürme potansiyeline sahiptir. Ancak bu dönüşüm, insan denetimi ve etik prensipler gözetilerek gerçekleşmelidir. İnsan-agent işbirliği modelleri, en başarılı sonuçları verecek ve gelecekteki otomasyon çözümlerinin temelini oluşturacaktır.

Bu hızla gelişen alanda güncel kalmak, teknoloji liderlerinin ve profesyonellerinin önceliği olmalıdır. AI agentları ve N8N gibi otomasyon araçlarının sunduğu fırsatları anlamak ve benimsemek, dijital dönüşüm yolculuğunda rekabet avantajı sağlayacağını düşünüyorum.

Author: Berke Düzgün

Push notifications are an essential feature of modern mobile apps, allowing businesses to engage users by sending timely updates, alerts, and offers. In React Native, Firebase Cloud Messaging (FCM) can be used for sending push notifications. With the help of react-native-firebase and Notifee, implementing this feature becomes more straightforward and powerful.

In this guide, I’ll walk you through the process of setting up Firebase Cloud Messaging within your React Native project. You’ll learn how to handle incoming push notifications, ensuring that your app can respond appropriately to messages sent from the cloud. Whether you’re sending alerts, updates, or personalized content, Firebase Cloud Messaging provides a robust solution to help you keep your users engaged and informed. Let’s dive into the world of push notifications in React Native and unlock the potential of FCM to enhance your app’s user experience.

“We must be willing to let go of the life we planned so as to have the life that is waiting for us.” — Joseph Campbell

Firebase Cloud Messaging is a cloud-based service that allows developers to send messages and notifications to users on various platforms, including iOS, Android, and web applications. By harnessing the capabilities of FCM, you can deliver personalized, timely content to your users, enhancing their overall experience with your app.

Prerequisites

Before starting, ensure you have the following:

• Basic knowledge of React Native and Firebase.

• Node.js and npm installed.

• A React Native app set up.

• Firebase project configured (if not, create one from the Firebase Console).

To accomplish what we need first we have to install some dependencies. We’ll use 3 different libraries for this.

yarn add @react-native-firebase/app

@react-native-firebase/messaging

react-native-permissions

@notifee/react-native

Configure Firebase in ioscd ios/ && pod install

To configure Firebase for iOS, we need to:

Add Firebase iOS SDK

• Download the GoogleService-Info.plist from the Firebase console.

• Drag and drop this file into your Xcode project, ensuring the “Copy items if needed” option is checked.

Modify iOS Project Settings

1. Set Deployment Target

In Xcode, set the deployment target to 11.0 or higher. This is required for Firebase Messaging and Notifee.

2. Enable Push Notifications

• Go to Signing & Capabilities in Xcode for your target.

• Add Push Notifications under the “Capability” section.

• Add Background Modes and enable Remote notifications.

Update AppDelegate.m

Open AppDelegate.m and modify it to support Firebase and Notifee notifications:

1. Import Firebase and Notifee

At the top of AppDelegate.m, add:#import <Firebase.h>

#import <RNCPushNotificationIOS.h>

2. Configure Firebase

In the didFinishLaunchingWithOptions method, initialize Firebase:- (BOOL)application:(UIApplication *)application didFinishLaunchingWithOptions:(NSDictionary *)launchOptions {

[FIRApp configure];

return YES;

}

Configure Firebase in Android

• Add your google-services.json file (from Firebase Console) to your android/app folder.

classpath ‘com.google.gms:google-services:4.3.10’

apply plugin: ‘com.google.gms.google-services’

Now we must request notification permissions from users to send push notifications. This can be done using the messaging module.import messaging from ‘@react-native-firebase/messaging’;

async function requestUserPermission() {

const authStatus = await messaging().requestPermission();

const enabled =

authStatus === messaging.AuthorizationStatus.AUTHORIZED ||

authStatus === messaging.AuthorizationStatus.PROVISIONAL;

if (enabled) {

console.log(‘Notification permission enabled.’);

} else {

console.log(‘Notification permission not granted.’);

}

}

Call requestUserPermission() during the app initialization.

The device needs a unique token to receive notifications. You can retrieve this token using the following code:import messaging from ‘@react-native-firebase/messaging’;

async function getFcmToken() {

const token = await messaging().getToken();

console.log(‘FCM Token:’, token);

}

useEffect(() => {

getFcmToken();

}, []);

This token will later be used to send notifications to specific devices from Firebase.

Firebase provides three scenarios to handle notifications: while the app is in the foreground, background, or terminated state.

• Foreground Notifications

To handle notifications in the foreground, you will use Notifee, a powerful library that allows you to show customized notifications when the app is active.import messaging from ‘@react-native-firebase/messaging’;

import notifee, { AndroidImportance } from ‘@notifee/react-native’;

messaging().onMessage(async (remoteMessage) => {

console.log(‘Message received in foreground:’, remoteMessage);

await notifee.displayNotification({

title: remoteMessage.notification.title,

body: remoteMessage.notification.body,

android: {

channelId: ‘default’,

importance: AndroidImportance.HIGH,

},

});

});

Notifee allows customization of notifications, such as adding images, custom sounds, and priority settings, which enhances the overall notification experience.

• Background and Terminated State Notifications

In the background, or terminated state, notifications are automatically handled by the system and appear in the notification tray. You can use Firebase’s built-in FCM message handling for this, so no additional code is needed for these states.

On Android, notifications are delivered through channels. You can configure channels with custom sounds, vibration patterns, and importance levels.

Before displaying a notification in Notifee, set up a channel:import notifee from ‘@notifee/react-native’;

async function createNotificationChannel() {

await notifee.createChannel({

id: ‘default’,

name: ‘Default Channel’,

importance: AndroidImportance.HIGH,

});

}

useEffect(() => {

createNotificationChannel();

}, []);

1. Sending a Test Notification

You can send test notifications from the Firebase Console by navigating to the Cloud Messaging section and sending a message to a specific device using the FCM token.

2. Handling Notification Clicks

Notifee also allows you to handle notification interaction (e.g., when the user taps on the notification).notifee.onBackgroundEvent(async ({ type, detail }) => {

if (type === notifee.EventType.ACTION_PRESS) {

console.log(‘Notification tapped: ‘, detail.notification);

}

});

Resources:

• React Native Firebase Documentation

Author: Mahir Uslu

In April 2024, the Bank for International Settlements (BIS) published an insightful article where its Chair, Agustín Carstens, emphasized the need for a future financial system that is both collaborative and interconnected. As global financial systems evolve, the need for an interconnected and accessible platform is more urgent than ever.

This blog explores the concept of the “Finternet” and highlights why promoting this vision is essential for the financial ecosystem. Imagine transferring assets instantly across borders without intermediaries. How would that change your financial transactions?

The Finternet is a novel financial concept introduced by the BIS. It envisions multiple interconnected financial ecosystems, much like the internet, designed to empower individuals and businesses by placing them at the center of their financial lives (Carstens & Nilekani, 2024). In essence, it is the “internet of finance world” encompassing payments, savings, borrowings, investments, insurance and more.

The core vision of the Finternet is to increase financial participation, provide personalized services, and improve both speed and reliability while reducing costs for end users. Central to this vision are people’s needs and challenges — without them, innovation would be unnecessary.

Today’s financial system still relies heavily on outdated legacy systems. Many financial systems have polished front-ends but outdated and flawed back-end infrastructures. Despite polished front-ends, these systems are plagued with issues like lengthy processes, security flaws, fragile performance, and manual dependencies. These problems result in slow operations, high costs, and a poor user experience, ultimately hindering accessibility and inclusiveness in financial services.

The challenge of unbanked and underbanked populations, especially in Emerging Markets and Developing Economies (EMDE), is compounded by low financial literacy. Many rely solely on cash and borrow from friends, family, or loan sharks at high interest rates. Without investment plans, insurance, or formal savings options, their money often remains “under the pillow.” This lack of access to financial services hampers their ability to boost incomes, enhance skills, and fully participate in the digital economy.

Due to this conjecture, we need an international and broader vision for future of the finance and that is Finternet. According to this vision, individuals and businesses would be able to transfer any financial asset they like, in any amount, at any time, using any device, to anyone else, anywhere in the world. Financial transactions would be cheap, secure and near-instantaneous (Carstens & Nilekani, 2024). With advancing technology, transforming this vision into reality is now more feasible than ever.

There are already increasing efforts to establish the Finternet, whether individuals are conscious of it or not. In recent decades, fintech firms have revitalized the sector with innovative solutions, reducing reliance on traditional banks and brokers and fostering a more dynamic competitive landscape. Although AI implementation is still in its early stages, it has significantly streamlined processes like Know Your Customer (KYC). Emerging open banking and money transfer apps are providing a more enjoyable user experience compared to traditional financial services. However, these advancements are limited, with nearly 1.4 billion people still excluded from the financial system. The key challenge is developing tools to unify the fragmented elements of the financial system. Despite all these efforts, the fragmented nature of the financial ecosystem remains a significant challenge.

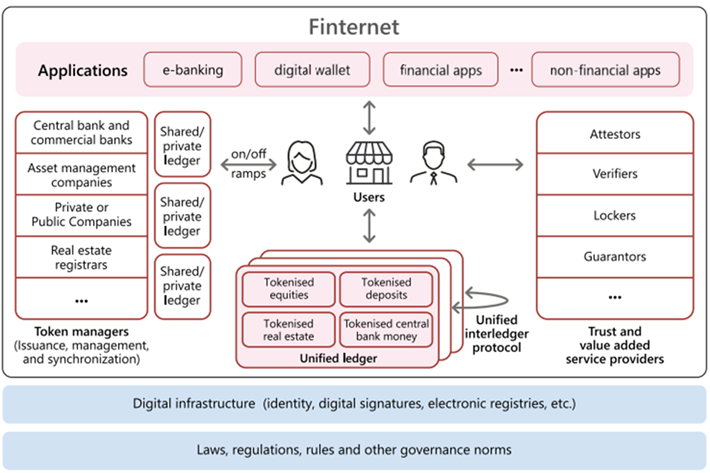

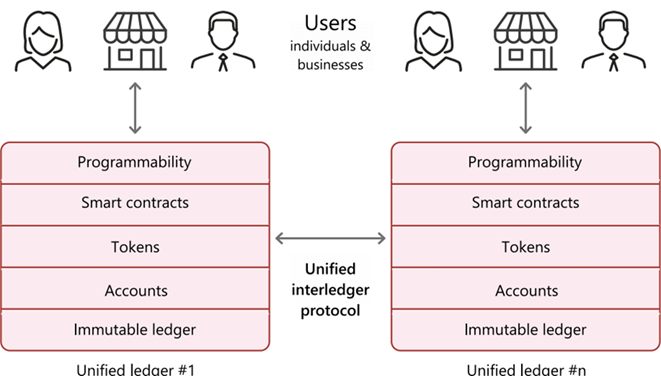

Therefore, it is essential to adopt a more expansive, cooperative and comprehensive vision for the future of the financial system in order to effectively meet the demands of the emerging economy. This future financial system will be token-based, supported by unified ledgers. Tokenization involves creating a digital representation of financial or real assets that reside on a programmable platform (Aldasoro et al., 2023). This process eliminates the distinction between the two, as all information necessary for the transaction of a financial asset — such as ownership, rules, and the logic governing transfers — resides in a single location. The adoption of tokenized financial assets has the potential to lighten many of the bottlenecks currently present in the financial system. The structure of the Finternet can be conceptualized as a series of building blocks (Image 1), with the unified ledgers containing digital representations of central and commercial bank money, along with other tokenized financial assets. Individuals and businesses would interact with the ledgers through their mobile or web applications in any time anywhere. Application Programming Interfaces (APIs) could facilitate the connectivity between these ledgers and other components of the financial system that operate outside the Finternet (Carstens & Nilekani, 2024).

The Unified Ledger (UL) serves as a platform for financial tools designed to manage tokenized assets in an organized, accessible, and secure manner. Numerous ULs may be established to address the varying needs of geographical areas, countries, societies, communities, institutions, and more. Each UL has a unique ID and can handle various tokenized assets such as currencies, equities, shares, deposits, real estate, copyrights, and artworks. Each of these ULs can utilize a Unified Interledger Protocol (UILP), similarly to the Internet’s TCP/IP (Transmission Control Protocol / Internet Protocol).

There are two main features of Unified Ledgers. First, they bring together everything needed to complete financial transactions like financial assets, ownership records, rules, and other important info into one place. Second, money and other financial assets are stored on the ledgers as executable objects, meaning they can be transferred electronically using pre-programmed “smart contracts” (Carstens & Nilekani, 2024).

A detailed exploration of the key characteristics of unified ledgers requires a careful look at various components, including programmability, smart contracts, tokens, and account management. Below, there is the architecture diagram for unified ledgers.

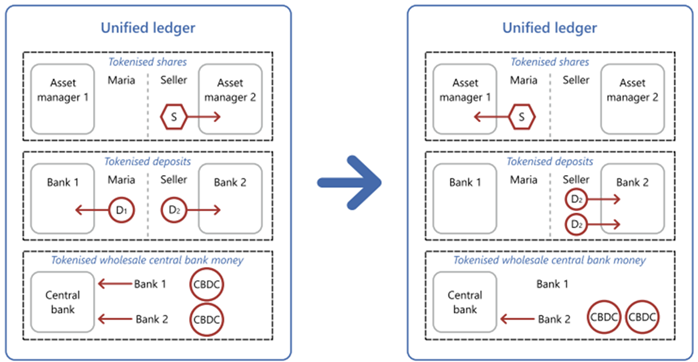

To better understand the concept of unified ledgers and tokenization, we can consider several use cases. For instance, if you wish to purchase a share of your preferred equity from your broker’s or bank’s mobile app but find that the stock price is significantly higher than your available investment amount. You may need to wait until you have sufficient funds. However, during this waiting period, you risk missing opportunities as prices may continue to rise. With tokenized assets on unified ledgers accessible through your broker’s app, you can acquire fractional shares without an extended waiting period. This approach democratizes investment opportunities for small investors, enabling them to build wealth with limited amounts and secure their future.

As a leader in digital transformation, Innovance is actively developing next-generation products and cutting-edge services to help bring the Finternet vision to life. We not only create solutions but empower our clients to be at the forefront of the future of finance.

We lead the way in helping you seize the future today.

We work diligently to develop applications that provide the most suitable and accurate solutions for your needs.

By sharing our pioneering expertise and knowledge, we provide effective tailored solutions to your unique challenges.

We ensure you gain the most valuable insights from your data.

We create unique designs and experiences that place the user at the center.

At Innovance, innovation is at the core of our brand identity. By continuously adapting to the latest technologies and regulatory landscapes, we are paving the way for the future of finance, aligning ourselves with the Finternet vision. Our dynamic team is here to guide you through every step of the journey.

The blog successfully presents the Finternet concept and how it addresses the limitations of current financial systems. Innovance’s commitment to innovation ensures that we play a critical role in shaping this future by delivering pioneering solutions and services.

Keywords: payment systems, financial system, financial intermediaries, financial instruments, currency, digital innovation, unified ledgers, tokenization, Innovance

Carstens, A., & Nilekani, N. (2024, April). Finternet: the financial system for the future. Bank for International Settlements: https://www.bis.org/publ/work1178.htm

Aldasoro, I, S Doerr, L Gambacorta, P Koo-Wilkens, and R Garratt (2023): “The tokenisation continuum”, BIS Bulletin, no 72.

Author: Berk Üstünel

Flutter 3.24 introduces a range of exciting updates that elevate app development to the next level. With this release, developers gain access to Flutter GPU for advanced graphics, multi-view embedding for web apps, and support for video ad monetization — powerful tools designed to help create versatile, high-performance applications.

A preview of Flutter GPU introduces advanced graphics capabilities, allowing developers to render complex 2D and 3D scenes directly within Flutter apps. This feature requires the Impeller rendering backend and is currently supported on iOS, macOS, and Android. While still in its early stages, Flutter GPU aims to extend support across all platforms, making it an invaluable asset for developers building visually rich applications.

This feature allows web applications to embed multiple Flutter views within different HTML elements simultaneously. With multi-view mode, developers can dynamically add or remove views, enabling more flexible and interactive web experiences. It’s particularly useful for integrating Flutter into larger, more complex web systems that require independent Flutter views.

Flutter now supports video ad monetization with the new Interactive Media Ads (IMA) plugin, enabling developers to seamlessly integrate video ads into their apps and unlock new revenue streams.

The initial release supports pre-roll ads on Android and iOS, with plans to extend to mid-roll ads in the near future.

The release introduces new slivers, such as PinnedHeaderSliver and SliverResizingHeader, to simplify the creation of dynamic app bars. Additionally, the new CarouselView widget in the Material library lets developers build scrolling lists where items resize dynamically based on their position.

The Cupertino library has undergone significant updates, introducing enhanced haptic feedback and improved customization options for CupertinoButton and CupertinoTextField. These changes bring Flutter’s iOS components closer to their native counterparts in terms of appearance and functionality.

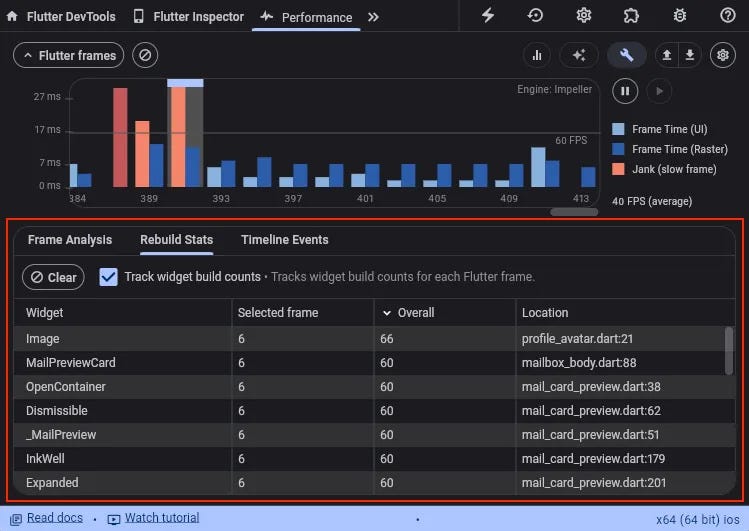

The DevTools suite received notable improvements, including the addition of Rebuild Stats, a feature that helps developers track widget rebuilds. This feature aids in identifying performance bottlenecks, allowing developers to optimize their apps more effectively.

Flutter now offers early support for Swift Package Manager, streamlining the management of iOS and macOS dependencies. This integration allows Flutter plugins to leverage the growing ecosystem of Swift packages, simplifying the setup process for Apple platforms.

This update brings notable performance enhancements, including better text rendering in the Impeller engine and improved defaults for downscaled images, ensuring that apps run smoothly across a wide range of devices.

Flutter 3.24 is a significant milestone in the evolution of Flutter, offering powerful new features that empower developers to create more dynamic, visually engaging, and high-performing applications. Whether you’re developing a game, a complex web app, or a traditional mobile app, Flutter 3.24 provides the tools and flexibility needed to bring your vision to life.

Author: Burak Dümer

In the ever-evolving landscape of European finance, traditional banks and financial institutions are facing an unprecedented challenge: the need to modernize and streamline their services to stay competitive and meet the escalating demands of tech-savvy customers. Enter Innovance’s cutting-edge banking platform — a game-changing solution designed to propel financial institutions into the digital age with unparalleled efficiency and customization.

The financial sector is at a critical juncture. With rapid technological advancements and shifting consumer expectations, banks must rethink their operational models. Gone are the days when a one-size-fits-all approach sufficed. Today’s consumers demand seamless, personalized banking experiences that can adapt swiftly to their evolving needs.

European financial institutions are under pressure to enhance their services for improved efficiency and customer satisfaction. The drive for digital transformation is not merely a trend but a necessity. Incumbent and challenger banks are in dire need of comprehensive solutions that offer high performance, fast time to market, and the ability to integrate best-of-breed technologies seamlessly.

As the financial sector continues to become increasingly digitized, the demand for flexible, end-to-end banking solutions has never been greater. Financial institutions are looking for ways to:

1. Enhance Efficiency: Streamline operations to reduce costs and improve service delivery by leveraging Straight Through Processing (STP).

2. Boost Customer Satisfaction: Offer a seamless, user-friendly banking experience.

3. Stay Competitive: Embrace digital transformation to remain relevant in a fast-changing market.

4. Integrate Best-of-Breed Technologies: Provide high-performance, tailored services through composable solutions.

Introducing Innovance’s Composable Banking Platform: The Ultimate Banking Ecosystem

Innovance offers a comprehensive banking solution designed to meet these exact needs. It provides a fully adaptable and composable banking ecosystem that can be tailored to the unique requirements of each financial institution.

Key Benefits of Innovance’s Banking Platform

· Composable Solutions for Tailored Banking Services

Financial institutions can integrate various best-of-breed solutions to create an end-to-end banking service that is uniquely their own. Whether it’s core banking, KYC, payments, or cards, Innovance’s Platform offers ready-to-use adapters for a wide range of vendors. This flexibility ensures that banks can offer high-performance, tailored services that align perfectly with their business goals and customer expectations.

· Seamless Integration through Powerful Middleware

At the hearth of Innovance’s solution is a powerful middleware platform. Designed for seamless integration across public and private clouds, it acts as a robust abstraction layer between your banking systems and external services providers. This scalable middleware allows for seamless integration between various banking components — such as KYC services, core banking systems, payment gateways, or card networks — without disrupting operations. By decoupling your systems from the specific of each provider, Innovance’s middleware ensures your bank can easily exchange components in a plug-and-play manner and therefore remain agile, scalable, and future-proof in an ever-evolving technological landscape.

· Cloud-Native Technologies for Enhanced Flexibility

Innovance’s platform leverages the power of cloud-native technologies to offer unmatched flexibility and scalability. By embracing the cloud, financial institutions can scale their operations effortlessly, ensuring they can handle increased workloads during peak times. Moreover, cloud-native solutions provide enhanced security and reliability, which are critical in the financial sector.

· Quick Setup and Deployment

Time is of the essence in the competitive banking industry. Innovance addresses this by offering a quick setup thanks to its ready-to-use adapters. These adapters facilitate rapid integration with different core banking systems, KYC solutions, payment gateways, and card providers. This means that banks can go to the market faster, delivering new services and features to their customers without lengthy development cycles.

· Mobile Banking Application for Modern Consumers

In today’s mobile-first world, a robust mobile banking application is no longer optional — it’s essential. Innovance’s platform includes a mobile banking application that can be tailored to specific business needs and to achieving desired user experience. This white-labeled solution ensures that banks can provide a seamless, intuitive, and personalized mobile banking experience to their customers. Whether it’s managing accounts, making payments, or accessing customer support, the mobile app covers all essential banking functions.

· Future-Proofing Your Banking Infrastructure

The financial landscape is constantly changing, and banks need solutions that can evolve with it. Innovance’s composable architecture enables banks to easily adapt to new technologies and market demands. Its flexible, cloud-native design allows banks to quickly adapt to new technologies and changing market demands, ensuring long-term viability and competitiveness in a rapidly changing industry.

· Enhancing Customer Satisfaction

Last but not least, Innovance’s solution is about enhancing customer satisfaction. By providing a comprehensive, vendor agnostic, and scalable banking ecosystem, financial institutions can deliver superior services that meet and exceed customer expectations. As a result, they achieve increased customer loyalty, higher engagement, and ultimately, greater profitability.

As European financial institutions navigate the path to digital transformation, solutions like Innovance’s composable banking platform will play a crucial role. By offering a fully customizable, scalable, composable ecosystem, Innovance empowers banks to meet the demands of the modern financial landscape head-on. It’s not just about staying competitive; it’s about leading the way.

If you’re a financial institution looking to revolutionize your banking services, Innovance is your ultimate partner in digital transformation. Discover how this end-to-end solution can help you stay ahead of the curve and deliver exceptional value to your customers.

Get in touch with Innovance today to learn more about their composable banking ecosystem and take the first step towards a brighter, more efficient future in banking.

In today’s business landscape, many enterprises are actively pursuing strategies to enhance sales performance through affordability solutions. Buy Now, Pay Later (BNPL) has emerged as a prominent option, providing interest-free credit, commission-free transactions, and flexible payment options for customers. By facilitating fast and seamless transactions and empowering consumers with increased purchasing power, BNPL not only meets the evolving demands of modern shoppers but also drives significant increases in sales volumes for businesses.

Buy now, pay later (BNPL) is a type of financing that allows consumers to make purchases and pay for them over time. It enables customers to spend beyond their monthly budget without having to pay the full price upfront in cash, debit, or credit card. By doing so, customers can finance their purchases immediately and repay them in fixed installments over time.

Merchants receive the full payment of the item in advance without having to manage the financing, depending on the deals between merchants and providers. They witness the growth of their sales due to the ease of payment provided by BNPL. BNPL providers handle underwriting customers, managing installments, and collecting payments, so the additional interest and fees directly go to these firms. This win-win situation not only provides ease of payment to consumers but also increases sales figures by activating the market.

BNPL services are typically offered as an option during the checkout process, alongside credit cards and other payment methods. When making a purchase, customers select a BNPL provider in the payment form and are then directed to the provider’s website or app to create an account or log in. Upon completion of the purchase, businesses receive the full payment upfront, though some agreements may extend the payment terms. Customers then pay their installments directly to the BNPL provider, which may include interest and fees.

Customers favor BNPL as a payment method for various reasons: the ability to make instant payments in-store without the need for a credit card or cash, quick and secure account setup, seamless and secure installment payments, and its applicability across diverse industries.

At Innovance, with our industry experience proven in more than 200 projects and our team of experts, we are here to support you with BNPL solutions. Innovance serves as a solution partner, offering an end-to-end BNPL solution that covers all processes, from customer onboarding to loan payments. Additionally, Innovance provides fast integration and setup processes, led by an expert team capable of handling custom requirements.

By streamlining these processes, Innovance ensures efficient and flexible backoffice management tailored to diverse business needs.

Innovance emerges as the premier partner for enterprises seeking to revolutionize their sales strategies through innovative affordability solutions such as BNPL. With a dedication to excellence, Innovance delivers seamless customer onboarding experiences, expedited integration processes, and a skilled team of experts ready to address unique needs.

Author: Ekinsel Akça & Ceren Eryılmaz

If you are looking for a starting point for SwiftUI, you are at the right place!

Similar to UIKit, some of the most used UI components exist in SwiftUI.

Text is equivalent to UILabel.Text(“Hello World!”)

.font(.title.bold())

.foregroundStyle(.blue)

As you guessed, Button is equivalent to UIButton.Button {

print(“Button Action”)

} label: {

Text(“Hello World!”)

.font(.title.bold())

.foregroundStyle(.white)

.padding()

.background(.blue)

.clipShape(RoundedRectangle(cornerRadius: 16))

}

As you might expect, Image is equivalent to UIImageView.Image(systemName: “house.fill”)

.resizable()

.scaledToFit()

.foregroundStyle(.blue)

TextField equals to UITextField.TextField(“placeholder”, text: .constant(“”))

.textFieldStyle(.roundedBorder)

When it comes to structuring the UI of your app, it’s essential to align views with one another.

In SwiftUI, there are two primary layout builders for this purpose: HStack and VStack.

These layout builders allow you to arrange views horizontally and vertically, respectively.

You can also combine them to achieve more complex layouts.

HStack aligns views horizontally.HStack {

Text(“Leading Text”)

.font(.body.bold())

.foregroundStyle(.blue)

Text(“Trailing Text”)

.font(.caption.bold())

.foregroundStyle(.orange)

}

It aligns views vertically.VStack {

Text(“Top Text”)

.font(.body.bold())

.foregroundStyle(.blue)

Text(“Bottom Text”)

.font(.caption.bold())

.foregroundStyle(.orange)

}

Spacer is SwiftUI’s light but powerful component to build flexible UI.

As you’re aware, aligning one view to another using constant margins (leading, top, trailing, bottom) can be overly cumbersome.HStack {

Text(“Leading Text”)

.font(.body.bold())

.foregroundStyle(.blue)

Spacer()

Text(“Trailing Text”)

.font(.caption.bold())

.foregroundStyle(.orange)

}

When a Spacer is placed between two Texts in an HStack, it naturally pushes the Texts towards the edges as it is designed to do.HStack {

Spacer()

Text(“Leading Text”)

.font(.body.bold())

.foregroundStyle(.blue)

Spacer()

Text(“Trailing Text”)

.font(.caption.bold())

.foregroundStyle(.orange)

Spacer()

Spacer()

}

I add one more Spacer before the Leading Text and two more Spacers after the Trailing Text.

When adding Spacers, the Leading Text is pushed away from its leading edge by one Spacer, while the Trailing Text is pushed away from its trailing edge by two Spacers.

As a result, the Trailing Text ends up farther away from the device edge compared to the Leading Text.

Regarding the data list, SwiftUI has two options, List or Foreach.

List equals to UITableView in UIKit.var numbers = [1, 2, 3, 4, 5]

List(numbers, id: \.self) { number in

Text(“\(number)”)

}

This is pure simple!

List also has some prepared UI such as divider, card-looking, etc.

var numbers = [1, 2, 3, 4, 5]

VStack {

ForEach(numbers, id: \.self) { number in

Text(“\(number)”)

}

}

The Foreach construct offers a leaner alternative to the List component. With Foreach, you have full control over building your list UI, resulting in a simpler and more customizable approach.

SwiftUI differs from UIKit by embracing the Declarative Programming approach.

In Declarative Programming, the UI observes changes in an Observable value or property.

Whenever the value changes, the UI dynamically adjusts to reflect the change.

SwiftUI’s fundamental property wrappers, State and Binding, enable observability:

State: Facilitates a one-way connection and is primarily used within the associated view.

Binding: Establishes a two-way connection and is utilized to transmit State properties to another view.

@State var text: String = “Initial Text”

VStack(spacing: 32) {

Button {

text = “Edited Change”

} label: {

Text(“Change Text”)

.font(.title.bold())

.foregroundStyle(.white)

.padding()

.background(.blue)

.clipShape(RoundedRectangle(cornerRadius: 16))

}

Text(text)

.font(.body.bold())

.foregroundStyle(.blue)

}

The Change Text button action modifies the observable text property. As the UI is designed to listen to changes in the text property, it automatically updates itself. This functionality is made possible by the State property wrapper.

Every SwiftUI view is a struct that conforms to the View protocol.

Since structs do not allow class inheritance, SwiftUI views can only conform to protocols.

These characteristics necessitate adopting an approach that views in SwiftUI are standalone and unique.

In UIKit, it is common practice to create base classes for specific views like UIViewController and UITableViewController. While it may be challenging to break away from this habit, it is possible with a shift in mindset!

One of SwiftUI’s core principles is less code, more work.

There are some ready-to-use view components to make development easier.

It is a mix of Image and Text in an HStack.Label(“I am a Label”, systemImage: “house.fill”)

It is a combined version of UISegmentedControl and UIPickerView.

It has various styles such as wheel, inline, segmented, and palette.let numbers = [1, 2, 3, 4, 5]

@State var selection: Int = 0

Picker(“Select”, selection: $selection) {

ForEach(numbers, id: \.self) { number in

Text(“\(number)”)

}

}

.pickerStyle(.inline)

Since SwiftUI’s inception, Apple has provided its image library, SF Symbols. You can effortlessly access these images from the library using the Image view.

Additionally, you have the flexibility to scale the image using the font function, similar to setting the font for a Text view.Image(systemName: “house.fill”)

.font(.largeTitle)

SwiftUI is a new way to develop projects in Apple’s environment.

You somehow adapt your thinking to SwiftUI’s way.

Once you can do that, the doors of SwiftUI will be open totally for you!

Author: Yusuf Demirci

With increased popularity among consumers in recent years due to its various expediencies, digital wallets in other words e-wallets, have replaced traditional payment methods like paper money and plastic cards and become an important part of digital transformation while allowing users to carry out financial transactions quickly, safely, and easily via digital platforms.

What is an e-wallet?

E-wallet serves as a prepaid account that allows users to make payments and transfer money, by digitally storing various payment methods within, such as debit and credit cards, bank accounts, and even cryptocurrencies. E-wallet providers in Türkiye are affiliated with the Central Bank of the Republic of Türkiye and are subject to the regulations it publishes.

How does it work?

First the user must register via either phone number or email. Next, the user is verified by personal information or through a KYC (Know Your Customer) process which often includes ID card verification with NFC scan and face recognition. Many wallet providers allow their users to use the application with some restrictions without any verification. The limitation on transaction amount and accessibility to the offered features may differ whether the user undergoes a verification process or not.

The user then connects their bank account to the digital wallet, either by linking it directly or by approving the creation of a new one by the wallet provider. Once connected, any funds added to the account will reflect in the wallet balance. Users may top up money from their bank account or use their credit or debit cards to do so. Users may also apply and receive loans from affiliated banks, depositing the amount into their e-wallets for future transactions. Either way, digital wallets ensure that card and bank account information, as well as personal data, are securely stored, typically transferring the related data encrypted.

The user is now able to purchase items, pay bills, transfer money to other accounts or pay for insurance while earning cashback in a fast, secure, and effortless way through their e-wallet. Services are often free or come with minimal transaction fees, providing an affordable option for users. The remaining balance can always be sent back to the bank account, it is up to the user’s preference.

E-wallet Solutions at Innovance

Examining the e-wallet solutions offered by Innovance allows us to identify the incentives that have contributed to the popularity of digital wallets in Türkiye.

Scalability: At Innovance, each e-wallet project, structured upon microservice architecture, yields unparalleled scalability and agility, reaching 1 million end-users and boasting an impressive daily active user count of 15,000. Our proficiency in technology equips us with extensive expertise, while our portfolio provides firsthand experience at the forefront. Here are some of our most well-known e-wallet projects, Vodafone Pay, Hayhay, Poca, Easycep and Başkent Kart. More projects are underway, reflecting our commitment to innovation and growth.

Fast Go to Market Time: Utilizing the modular feature set and responsive framework inherent in our white label solutions, along with tailor-made solutions, a new multilanguage e-wallet project can be customized and swiftly introduced to digital distribution platforms such as the App Store, Google Play Store and App Gallery in less than two months.

Safe and Secure: Since wallet providers rely on the trust of the users, we offer well-defined security measures. Our digital wallet solutions bring forth integrated two factor authentication to reduce fraud and tokenization to mitigate the risk of security breaches. Each wallet project within our portfolio undergoes penetration testing — a process where cybersecurity experts simulate real-world attacks to identify vulnerabilities. This meticulous approach ensures not only a profound understanding of our systems but also fortifies the security posture of our digital wallets.

Convenient and Fast: E-wallets offer contactless transactions via mobile devices, allowing users to withdraw money from ATMs, top up funds, make payments, and conduct seamless peer-to-peer (P2P) transfers by simply scanning a QR code or entering recipient details. Additionally, e-wallets provide access to personal loan services from partnered banks directly through the platform, enabling users to apply for and receive loans instantly like in Hayhay project. This feature allows users to conveniently access and spend loaned amounts directly from their e-wallets, enhancing platform utility.

Loyalty Cashback: E-wallets often integrate loyalty programs and cashback rewards to incentivize users to make purchases using the platform. Users may earn points or cashback for every transaction made with the e-wallet. For example, when users make fuel purchases using their e-wallets, like they do in Poca, they can earn points or cashback rewards. These rewards accumulate based on the amount spent on fuel, and users can then redeem them as cashback for future purchases, effectively saving money on their transactions.

Promotions and Discounts: E-wallet providers collaborate with merchants to offer exclusive promotions and discounts to users who opt to make payments through their platform. These incentives range from special discounts on products or services to bonus rewards and limited time offers. For instance, an e-wallet provider might define a campaign for Mother’s Day, offering cashback returns on every transaction made through the platform during the specified period like in the campaigns Poca offers.

Paying for Insurance or Invoices: Some e-wallets like Başkent Kart and Vodafone Pay, also allows users to pay for insurance premiums or invoices such as electricity or phone bills directly through the app. Users can securely store their payment information within the e-wallet and set up recurring payments for bills or subscriptions, streamlining the payment process and ensuring timely payments.

E-wallets offer various benefits, from enhanced security protocols to enticing rewards, ultimately redefining the management of transactions while enriching the user experience in a modern manner. Innovance’s innovative solutions have accelerated their adoption, offering scalability, fast deployment, robust security, and convenient modular features. As technology evolves, e-wallets will continue to shape the future of digital finance.

Author: Melis Ergen

Lean Business Analysis is focused on increasing efficiency by making incremental improvements to software and capturing customer feedback early and often. This minimizes waste in the product development cycle. Lean Business Analysis prioritizes experimentation over elaborate planning, and celebrates continuous, incremental improvement. It eliminates much of the bureaucracy that accompanied traditional Business Analysis.*

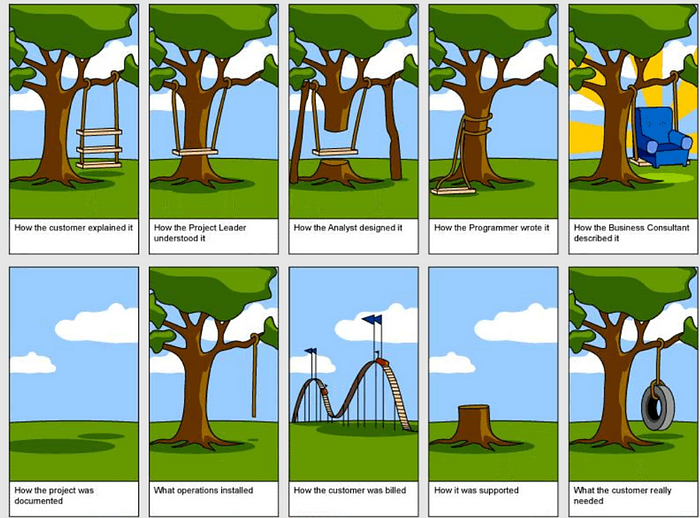

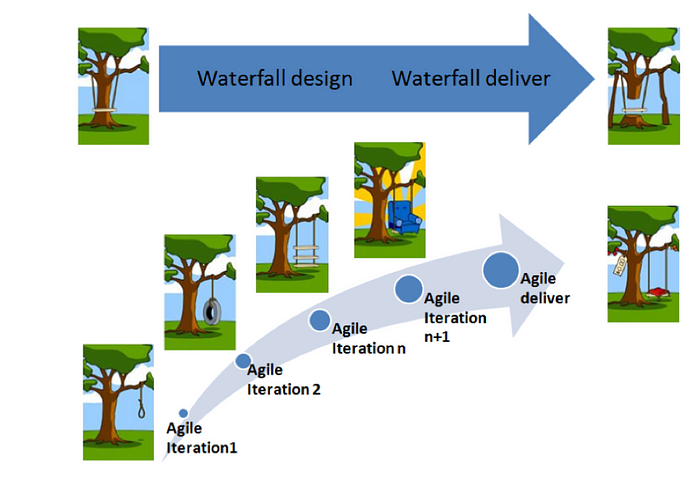

It can easily explained by the famous image below. We will see that we are on the right track if we regularly develop and test the small parts and requirements of the project and get customer feedback at every step.

The answer will be the cost of the project. The most important goal is to fulfill the necessary needs and demands that the customer will use when the project is completed.

In fact, this is one of the foundations of the Lean approach. After Henry Ford switched to the Lean Manufacturing system in 1913 to increase mass production, Eiji Toyoda took this systematic one step further in the 1950s and contributed to its current state. Among its basic principles is the article “An approach that eliminates unnecessary resource consumption (does not add value to the organization) in production and other processes”.

The answer will be time. Applying Agile and Lean thinking along with detailed requirements discovery, analysis, and acceptance testing to your software development process will help the IT requirements definition process evolve rapidly.

In the analysis processes, faster progress is supported with small comprehensive user stories that bring together small and meaningful pieces instead of comprehensive user stories that produce meaningful outputs as a result of long researches and plans.

In an ever-changing world, we can find the answer in accepting that requirements are constantly changing. For example, advancing the waterfall method, which is one of the traditional business analysis models, may cause the following problems;

· Misunderstanding of the requirement

· Incorrect analysis of the requirement

· Change of requirement over time

However, with the Lean analysis approach, it is possible to detect and prevent many of these problems at an early stage.

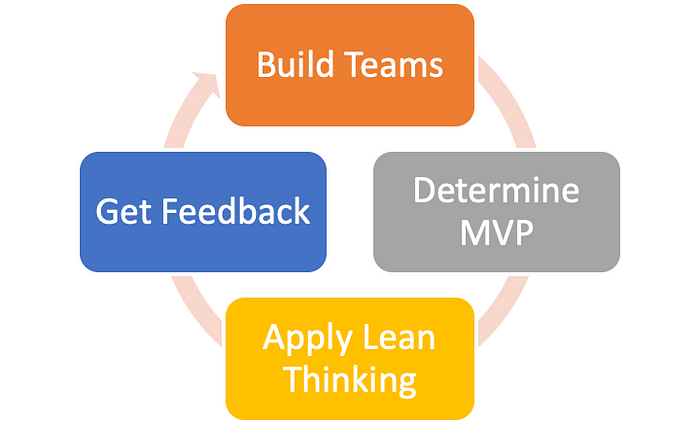

· Have a team that can organize its own work and is open to communication.

· One of the other most important things is to set a minimum viable product (MVP) and a PBL clearly clarifies user stories and acceptance criteria.

· Apply Lean Thinking is one of the most important foundations. Thus, by applying the Lean approach, we prevent too much time loss that may arise in the above question and answer content.

· Get feedback. Conducting continuous testing and receiving feedback from the Product owner and customers will help us understand that we are on the right track.

In a rapidly changing world, we must also change our traditional approaches.

We can use the lean analysis approach for any applicable requirement, without forgetting that time and cost are the most important determinants due to the nature of every business.

In this method, which we are generally loyal to, we can create analysis models suitable for us and perform needs analysis faster with methods such as 5n1k. All the issues questioned above are to understand the need correctly, to minimize unnecessary costs and to produce useful outputs.

Analysis is key as it is one of the early stages of development processes. We should not forget that it is always important to move forward with correct and understandable lean analyzes without forgetting that a wrong analysis leads to a wrong development, a wrong test, and as a result turns into an unacceptable business requirement.

· businessanalysisexperts.com :An Overview of Lean / Agile Business Analysis

Author: Pınar Candan