Software Development

What is Finternet

November 26, 2024

A Vision for the Future Financial System

In April 2024, the Bank for International Settlements (BIS) published an insightful article where its Chair, Agustín Carstens, emphasized the need for a future financial system that is both collaborative and interconnected. As global financial systems evolve, the need for an interconnected and accessible platform is more urgent than ever.

This blog explores the concept of the “Finternet” and highlights why promoting this vision is essential for the financial ecosystem. Imagine transferring assets instantly across borders without intermediaries. How would that change your financial transactions?

What is Finternet and why we need it right now?

The Finternet is a novel financial concept introduced by the BIS. It envisions multiple interconnected financial ecosystems, much like the internet, designed to empower individuals and businesses by placing them at the center of their financial lives (Carstens & Nilekani, 2024). In essence, it is the “internet of finance world” encompassing payments, savings, borrowings, investments, insurance and more.

The core vision of the Finternet is to increase financial participation, provide personalized services, and improve both speed and reliability while reducing costs for end users. Central to this vision are people’s needs and challenges — without them, innovation would be unnecessary.

Today’s financial system still relies heavily on outdated legacy systems. Many financial systems have polished front-ends but outdated and flawed back-end infrastructures. Despite polished front-ends, these systems are plagued with issues like lengthy processes, security flaws, fragile performance, and manual dependencies. These problems result in slow operations, high costs, and a poor user experience, ultimately hindering accessibility and inclusiveness in financial services.

The challenge of unbanked and underbanked populations, especially in Emerging Markets and Developing Economies (EMDE), is compounded by low financial literacy. Many rely solely on cash and borrow from friends, family, or loan sharks at high interest rates. Without investment plans, insurance, or formal savings options, their money often remains “under the pillow.” This lack of access to financial services hampers their ability to boost incomes, enhance skills, and fully participate in the digital economy.

Due to this conjecture, we need an international and broader vision for future of the finance and that is Finternet. According to this vision, individuals and businesses would be able to transfer any financial asset they like, in any amount, at any time, using any device, to anyone else, anywhere in the world. Financial transactions would be cheap, secure and near-instantaneous (Carstens & Nilekani, 2024). With advancing technology, transforming this vision into reality is now more feasible than ever.

There are already increasing efforts to establish the Finternet, whether individuals are conscious of it or not. In recent decades, fintech firms have revitalized the sector with innovative solutions, reducing reliance on traditional banks and brokers and fostering a more dynamic competitive landscape. Although AI implementation is still in its early stages, it has significantly streamlined processes like Know Your Customer (KYC). Emerging open banking and money transfer apps are providing a more enjoyable user experience compared to traditional financial services. However, these advancements are limited, with nearly 1.4 billion people still excluded from the financial system. The key challenge is developing tools to unify the fragmented elements of the financial system. Despite all these efforts, the fragmented nature of the financial ecosystem remains a significant challenge.

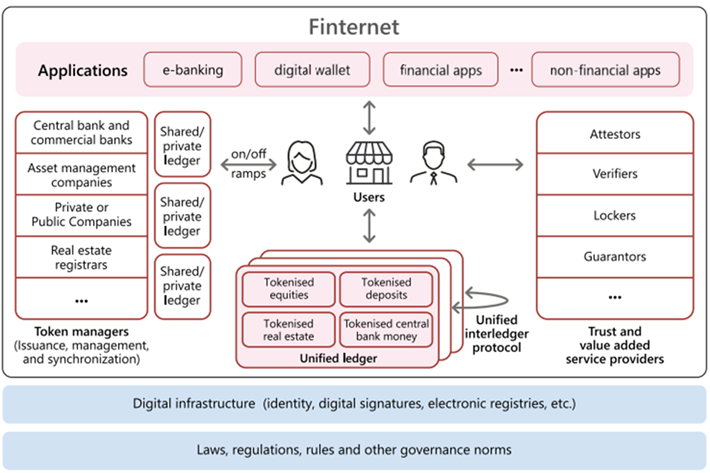

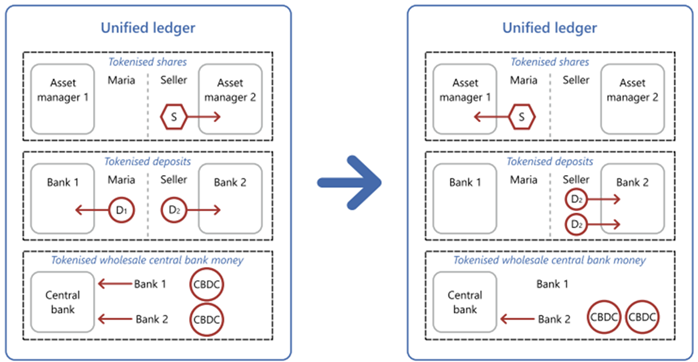

Therefore, it is essential to adopt a more expansive, cooperative and comprehensive vision for the future of the financial system in order to effectively meet the demands of the emerging economy. This future financial system will be token-based, supported by unified ledgers. Tokenization involves creating a digital representation of financial or real assets that reside on a programmable platform (Aldasoro et al., 2023). This process eliminates the distinction between the two, as all information necessary for the transaction of a financial asset — such as ownership, rules, and the logic governing transfers — resides in a single location. The adoption of tokenized financial assets has the potential to lighten many of the bottlenecks currently present in the financial system. The structure of the Finternet can be conceptualized as a series of building blocks (Image 1), with the unified ledgers containing digital representations of central and commercial bank money, along with other tokenized financial assets. Individuals and businesses would interact with the ledgers through their mobile or web applications in any time anywhere. Application Programming Interfaces (APIs) could facilitate the connectivity between these ledgers and other components of the financial system that operate outside the Finternet (Carstens & Nilekani, 2024).

What is Unified Ledger?

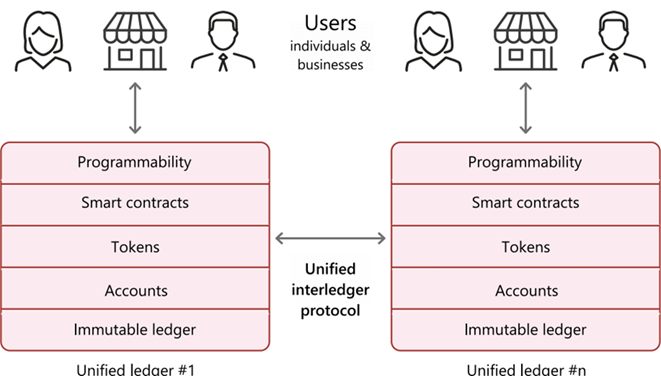

The Unified Ledger (UL) serves as a platform for financial tools designed to manage tokenized assets in an organized, accessible, and secure manner. Numerous ULs may be established to address the varying needs of geographical areas, countries, societies, communities, institutions, and more. Each UL has a unique ID and can handle various tokenized assets such as currencies, equities, shares, deposits, real estate, copyrights, and artworks. Each of these ULs can utilize a Unified Interledger Protocol (UILP), similarly to the Internet’s TCP/IP (Transmission Control Protocol / Internet Protocol).

There are two main features of Unified Ledgers. First, they bring together everything needed to complete financial transactions like financial assets, ownership records, rules, and other important info into one place. Second, money and other financial assets are stored on the ledgers as executable objects, meaning they can be transferred electronically using pre-programmed “smart contracts” (Carstens & Nilekani, 2024).

A detailed exploration of the key characteristics of unified ledgers requires a careful look at various components, including programmability, smart contracts, tokens, and account management. Below, there is the architecture diagram for unified ledgers.

To better understand the concept of unified ledgers and tokenization, we can consider several use cases. For instance, if you wish to purchase a share of your preferred equity from your broker’s or bank’s mobile app but find that the stock price is significantly higher than your available investment amount. You may need to wait until you have sufficient funds. However, during this waiting period, you risk missing opportunities as prices may continue to rise. With tokenized assets on unified ledgers accessible through your broker’s app, you can acquire fractional shares without an extended waiting period. This approach democratizes investment opportunities for small investors, enabling them to build wealth with limited amounts and secure their future.

What Role Does Innovance Play in Realizing the Finternet Vision?

As a leader in digital transformation, Innovance is actively developing next-generation products and cutting-edge services to help bring the Finternet vision to life. We not only create solutions but empower our clients to be at the forefront of the future of finance.

Digital Transformation

We lead the way in helping you seize the future today.

- Digital Banking

- Micro Services

- Core / Back-End Services

- Open-Banking

Digital Applications

We work diligently to develop applications that provide the most suitable and accurate solutions for your needs.

- Innovance Wallet As A Service Platform

- Alternative Distribution Channels

- Platform Design & Development

- Application Design & Development

Technology Advisory

By sharing our pioneering expertise and knowledge, we provide effective tailored solutions to your unique challenges.

Data Consultancy

We ensure you gain the most valuable insights from your data.

Design Studio

We create unique designs and experiences that place the user at the center.

At Innovance, innovation is at the core of our brand identity. By continuously adapting to the latest technologies and regulatory landscapes, we are paving the way for the future of finance, aligning ourselves with the Finternet vision. Our dynamic team is here to guide you through every step of the journey.

Conclusion

The blog successfully presents the Finternet concept and how it addresses the limitations of current financial systems. Innovance’s commitment to innovation ensures that we play a critical role in shaping this future by delivering pioneering solutions and services.

Keywords: payment systems, financial system, financial intermediaries, financial instruments, currency, digital innovation, unified ledgers, tokenization, Innovance

Resources

Carstens, A., & Nilekani, N. (2024, April). Finternet: the financial system for the future. Bank for International Settlements: https://www.bis.org/publ/work1178.htm

Aldasoro, I, S Doerr, L Gambacorta, P Koo-Wilkens, and R Garratt (2023): “The tokenisation continuum”, BIS Bulletin, no 72.

Author: Berk Üstünel